COG Group volumes increased 16% in FY24. This growth was driven by strong new broker acquisition (12%) and solid organic (4%) growth. At over $8.9b, our annual volumes offer solid insights into activity within the asset finance market, for both brokers and lenders. So, let’s look within these numbers to find the key themes from FY24.

1. Growth rates have settled slightly from prior years.

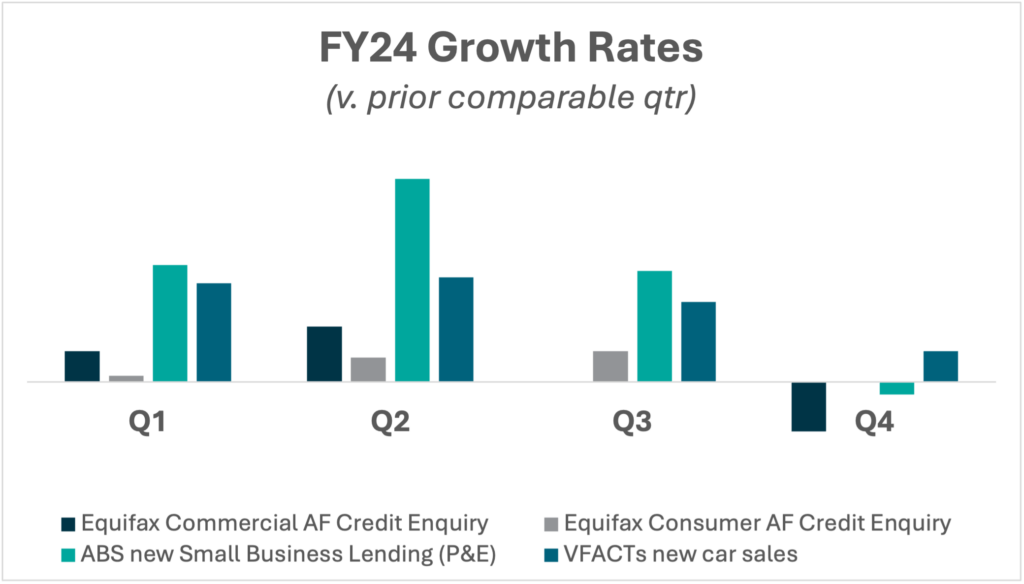

FY24 got off to a slow start, bounced back over quarters 2 and 3, before flattening off in Q4. This is reflected in some common indexes used to track activity in our segment.

In fact, we can see on most measures, the June quarter this year was materially down on the prior June quarter. The Equifax commercial enquiry index was -8%, whilst COG Brokers on a like-for-like basis (where we are excluding new brokers to the group) were -5% in June.

Looking within the VFACTS trend, we expect the strong new vehicles sales over the first 9 months came at the expense of used vehicle sales, as buyers that held out for new stock over COVID took deliveries – this is particularly the case for fleets and government, noting whilst overall sales were -4% in June, sales to Government were +34%.

Likewise, the trend in Consumer Credit Enquiry may also overstate underlying settlements.Anecdotally consumer applicant credit quality is dropping, which is to be expected with rising rates and cost of living stress – so whilst there may have been more applicants, the conversion to settlements is lower.

Keeping things in context…

When comparing FY24 numbers against FY23 it is important to recognise how extraordinary the end to FY23 was. Asset purchases were brought forward to take advantage of lucrative tax incentives, including Temporary Full Expensing and a far larger Instant Asset Write-Off threshold. These drivers made June 2023 volumes the highest on record: ABS Small Business New Lending data for Plant Equipment had June 2023 eclipsing the prior record month by 21%, and again COG brokers out-shot the market by beating their prior record by 30%. FY24, by comparison, was only supported by the nominal $20k Instant Asset Write-Off.

2. Unseasonable 2nd half

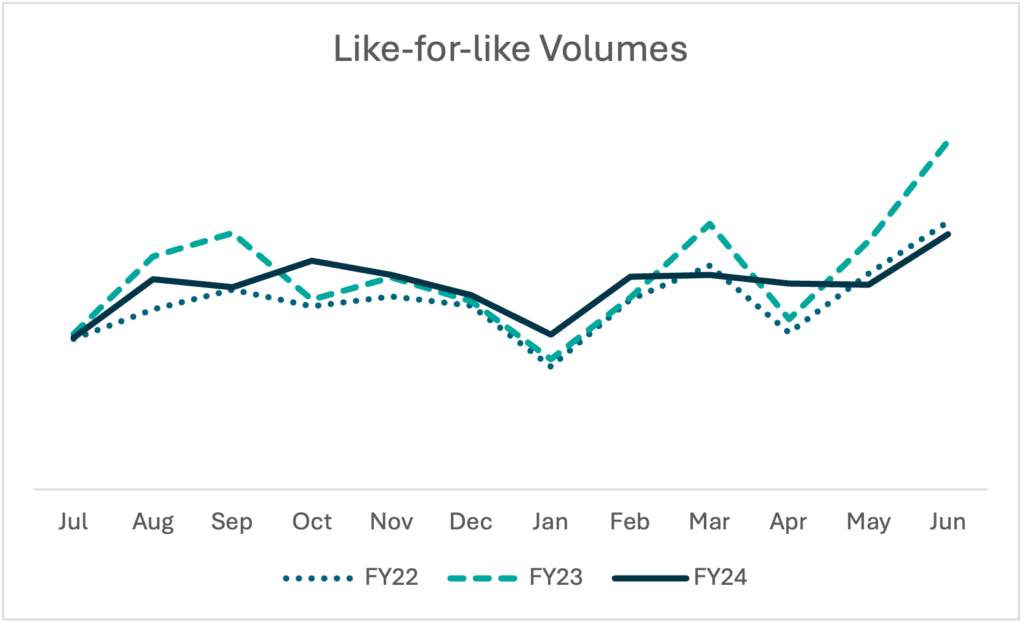

Seasonality in Asset Finance is normally predictable: the first half is relatively steady, producing 48% of the volume, while the second half is characterized by a large March, a rest in April, before heading to the summit over May and June.

This financial year was different. As we see below (again using like-for-like data), volumes were much more even throughout the financial year – in particular the 2nd half lacked the usual peaks and troughs.

In part we can point to the early occurrence of Easter, but we also believe we are seeing the trailing impacts of the aggressive tax incentives introduced over COVID:

Lower accelerated depreciation allowances decrease the incentive to bring forward investments in plant & equipment.

Businesses that took advantage of Temporary Full Expensing now hold P&E fleets that are written down to zero, meaning any replacement of these assets will likely result in significant profits on asset sales.

Company profits may not be as large as in prior years, resulting in less tax-driven timing of asset purchases.

Indeed, anecdotally we had numerous brokers telling us of clients delaying purchases until the start of the new financial year – a far cry from the normal EOFY rush.

3. Return of the banks

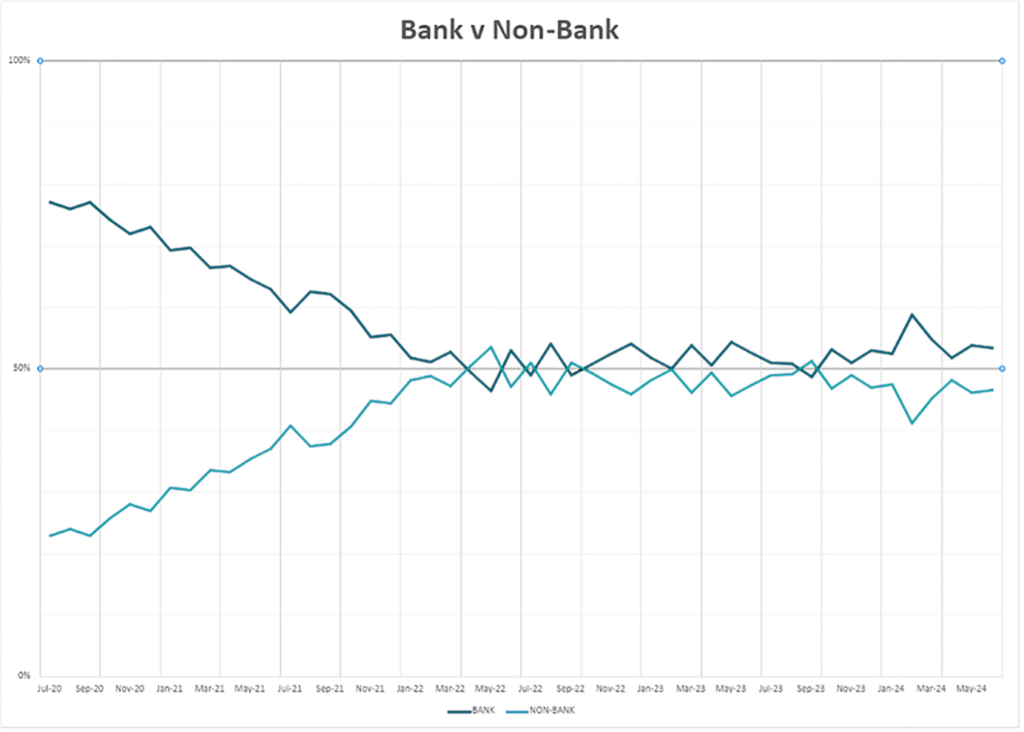

COG’s bank v non-bank market share tracker broke from the trend early in FY24. Whereas non-banks had enjoyed parity over FY22 and FY23, peaking as high as 54% in mid-2022, share has now swung back to the banks.

Non-bank share has settled around 47%, after falling as low as 41% in Feb-24, corresponding with Metro’s outage and Macquarie’s final push prior to exiting the market.

The main beneficiary of these trends has been the Westpac Group, which increased its portion of COG Group volumes to 24% in FY24 (21% FY23). NAB has also seen material growth over FY23, predominantly in the larger ticket space.

The key driver has been rates, with the spread of ‘delivery rate’ (base rates adjusted for differences in distributor remuneration) between non-banks and banks having widened in line with tightening monetary policy – put simply costs for deposits have not increased at the same rate as costs for wholesale funding.

Other contributing factors are the reduction in bank turnaround times, which peaked over COVID; the settling out of major bank KYC procedures (or, more specifically the increasing portion of broker clients now verified with banks); and reduced heat in the market, resulting in clients spending more time shopping for the leanest deal, rather than the most efficient answer.

In Summary

FY24 presented a different set of circumstances to prior years. Increased interest rates and inflation saw demand for assets slow, and reduced government incentives, had an impact on purchase timing triggers.

But overall, the asset finance industry continued to weather the headwinds. While margins were squeezed and growth was harder to come by than in previous years, average volumes remained consistent for brokers over the 12 months. This is a great result when we consider the strength of the headwinds at play.

Given we are much nearer the top of the rate cycle than the bottom, we remain optimistic that demand for vehicle, equipment and SME funding will continue across various industries. That demand will be met by brokers with the specific expertise, tools and market access required to meet customer needs – fueling the success of AF brokers in FY25.

Interested to learn more about how COG can offer the scale and stability to support your asset finance business? Contact our team for an obligation-free chat today.