ABS CAPEX Data Shows Growth for Plant & Equipment Sector

2 min read

The latest Australian Bureau of Statistics (ABS) data on private sector capital expenditure (CAPEX) for the September 2024 quarter reveals a nuanced picture of economic activity. While overall investment in plant and equipment continues to climb, the drivers of this growth highlight key shifts within the Australian economy.

Services sectors such as Media & IT, Financial & Insurance Services, and Health Care are leading the charge, while manufacturing makes a notable comeback with clean energy adaptations. However, not all industries are experiencing the same momentum, with some sectors showing signs of slowing investment.

Let’s delve into the data and unpack the trends shaping Australia’s economic landscape and how it effects asset finance brokers.

Highlights: Plant & Equipment CAPEX Sept Qtr 2024

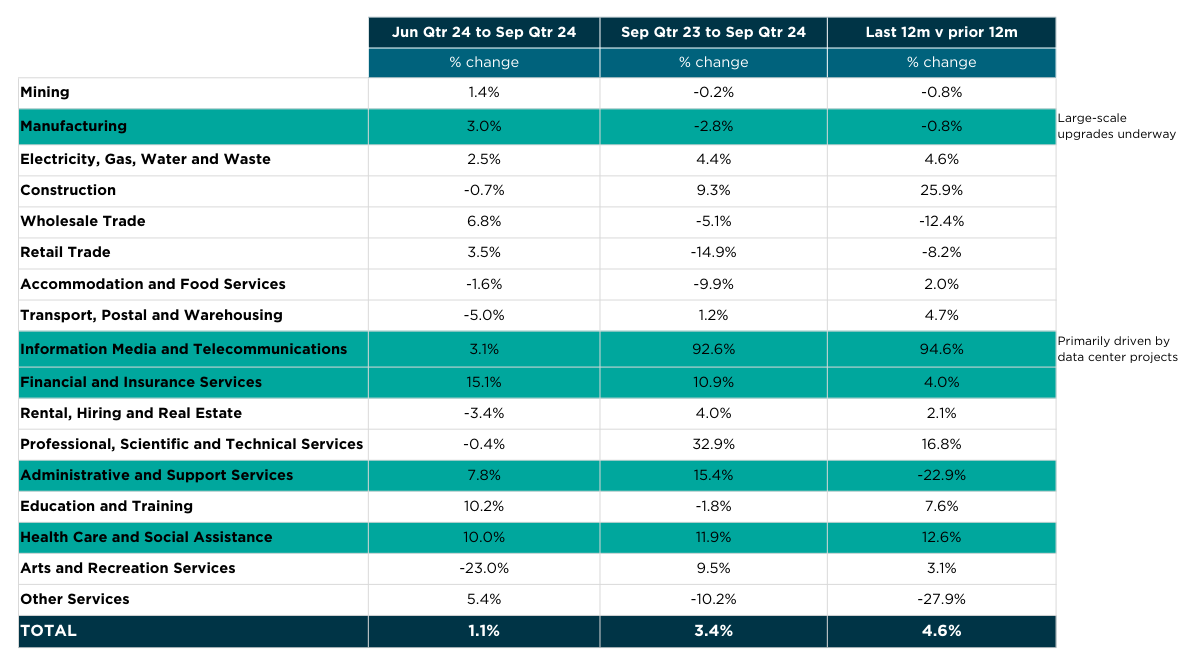

+1.1% growth on the prior quarter:

Driven by Services sectors: Media & IT (+3.1%), Financial & Insurance Services (+15.1%), Admin & Support (7.8%), and Health Care & Social Assistance (+10%).

Manufacturing also returned to growth (+3%), driven by large-scale upgrades that are underway, including to adapt to cleaner energy technology.

Sep-24 qtr +3.4% on the prior Sept-23qtr, and last 12m +4.6% on the prior 12m.

Looking back over the prior 12m we see P&E CAPEX in the Construction, and Transport and Warehousing sectors slowing; along with Rental, Hiring and Real Estate; and Arts & Recreation.

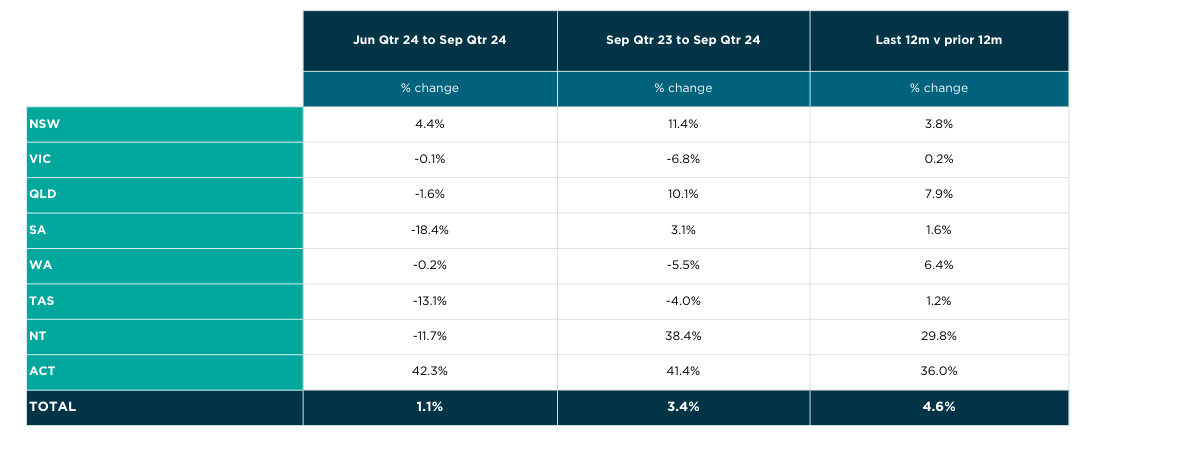

When looking at location, we see sharp drop-offs in P&E CAPEX in the smaller states (SA -18%, Tas -13%, and NT -12%), Vic and WA still flat, a dip in Qld (-2%) off the back of some good growth in prior quarters, and NSW still the strongest (+4.4%), with the ACT in particular continuing its very strong growth (+42%).

The data showed a strong uplift in outlook, with the overall 2024-25 P&E CAPEX Estimate raised by 8.7%, compared to the prior estimate.

What does this mean for Asset Finance Brokers?

Overall, these figures reflect what our member base is seeing – the market continues to grow, albeit slowly and somewhat erratically from industry to industry, and across locations. The uplift in CAPEX forecasts is very positive and paired with rates potentially coming off a peak in the next 6 months, should deliver strong volumes.

New Opportunities

It is also worth noting new opportunities for AF brokers and lenders within the services sector, particularly with traditional customers in transport and construction off a little.

Whilst these service sectors may not be traditional AF clients, these latest figures show that they do present real opportunities, as they are currently investing heavily in vehicles, transport equipment, racking and handling equipment, fitouts, and generally re-tooling facilities and operations.

A complete and strong panel is imperative to capture these opportunities and best-serve clients.